- Home

- /

- Thailand-landing-2020

- /

- Thailand – Taxation Structure

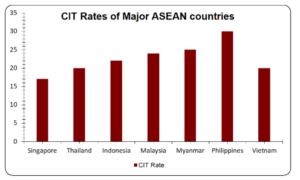

Corporate Income Tax (CIT)–The prevailing standard CIT rate in Thailand is 20%. A comparative overview of seven major ASEAN economies, as seen in the chart below, indicates that Thailand’s CIT rate is not only below the average but is also one of the lowest among these markets. This makes Thailand one of the most tax amicable countries in ASEAN.

Further, for foreign companies not carrying on business in Thailand a final withholding tax (WHT) is levied on certain types of assessable income (e.g. interest, dividends, royalties, rentals, and service fees) paid from or in Thailand. The rate of tax is generally 15%, except for dividends, which is 10%, while other rates may apply under the provisions of a double tax treaty (DTT).

For information on Petroleum Income Tax and Rates for companies with low paid-in capital and income, refer to the link below:

https://taxsummaries.pwc.com/thailand/corporate/taxes-on-corporate-income

Personal Income Tax (PIT) – The PIT rates for individual income are as follows:

* Converted to US$ from THB